The GDV Problem

The stale valuation problem

At origination, a RICS valuer inspects the site, reviews comparable sales, and produces a GDV figure. That figure underpins the LTGDV covenant, the LTV calculation, the Article 124K risk weight eligibility, and the exit assumption that justifies the whole loan.

That valuation is a point-in-time snapshot. By the time the loan completes, the market has moved. Comparable sales have changed. Local planning decisions have been made. Interest rates have shifted. The GDV figure in the credit paper may be materially different from what the completed units would actually sell for today.

Most ADC loans run for 12-18 months. A lot can change in 12-18 months. The lender typically doesn't revalue until the loan is up for extension or there's a specific trigger event. Between origination and that point, the GDV assumption in the credit model is not being tested against live market data.

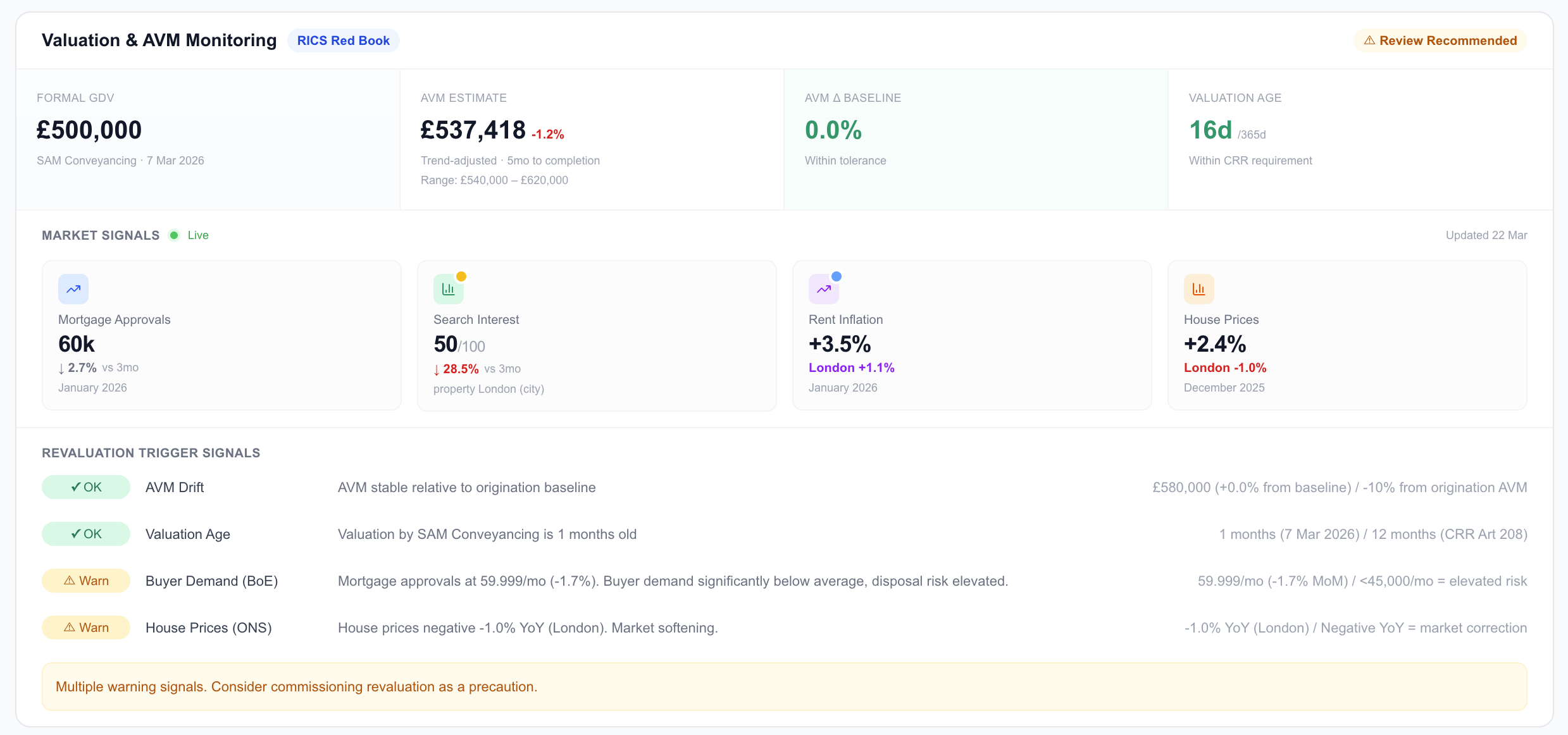

If GDV drops 8% during the loan lifecycle and LTGDV was originally 68%, the covenant-compliant position is now 73.9% on the same loan amount. If the covenant threshold is 75%, the lender is approaching a breach they don't know about yet because no one has revalued the asset.

Three ways GDV drift creates hidden risk

1. LTGDV covenant drift

The facility agreement sets an LTGDV covenant at, say, 70%. At origination, GDV is £3m and the loan is £2m, so LTGDV is 66.7%. The lender is comfortable.

Over the following eight months, comparable sales in the local market soften by 7%. GDV is now realistically £2.79m. LTGDV on the same loan is now 71.7%. The covenant has been breached. The borrower hasn't reported it because they're not required to revalue mid-loan. The lender doesn't know because no one is watching comparable sales between formal revaluations.

2. Article 124K eligibility erosion

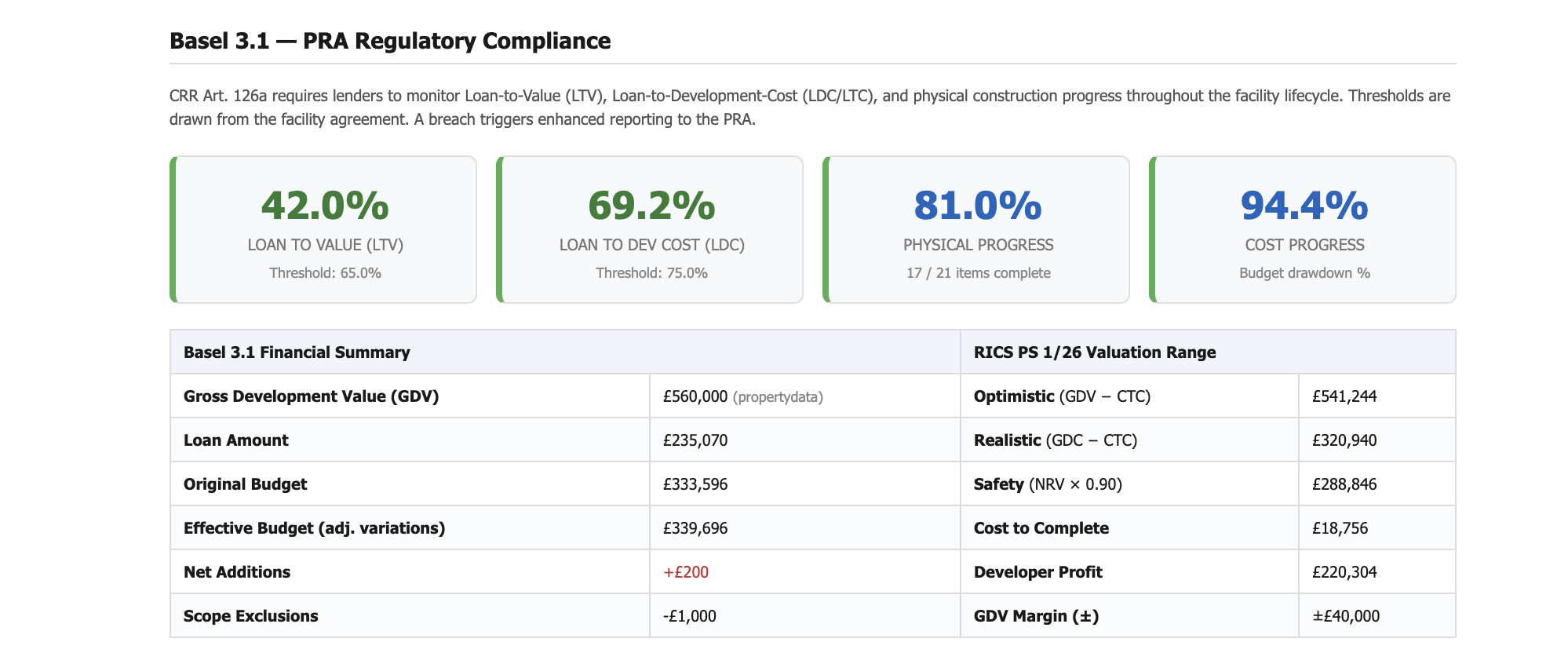

Basel 3.1 PS1/26 sets conditions for the 100% risk weight on ADC exposures. One of those conditions relates to LTV against the completed value. If GDV drift pushes the real LTGDV above the threshold, the exposure should be reclassified and the risk weight rises to 150%.

Without continuous market monitoring, the lender continues to hold the exposure at 100% risk weight based on a GDV figure that no longer reflects market conditions. This is a capital adequacy issue, not just a covenant issue.

3. Exit assumption risk at the back end

The exit strategy assumes the completed units sell at or near the GDV. If the market has moved materially during the build, the units may sell below the level needed to repay the loan in full. The lender discovers this at exit, when there are no good options. Monitoring GDV continuously means seeing that risk building during the loan, when there are still choices: early sales, price adjustment, extended marketing period, facility restructure.

What continuous market monitoring means in practice

Revaluing every asset every quarter is not practical or cost-effective. But comparable sales data, planning decisions, and macro market indicators are available continuously. The question is whether that data is being applied to the live portfolio systematically.

Three data streams that give a continuous GDV picture without a formal RICS revaluation:

1. Land Registry comparable sales, refreshed automatically

Land Registry transaction data is published with a lag but is comprehensive. Comparable sales within a defined radius and property type, refreshed as new transactions are registered, give an ongoing picture of where actual market prices are relative to the GDV assumption at origination. A 5% movement in comparables is a signal. A 10% movement is a covenant review trigger.

2. Local planning activity

A major planning approval for a competing development nearby, or a refusal that affects supply, changes the exit environment. Planning portal data can be monitored automatically for the postcode areas relevant to each loan in the portfolio. A lender who knows about a 200-unit planning approval 0.8 miles away before it's in the news has time to reassess the exit assumption.

3. Macro stress-testing applied live

BoE base rate changes, ONS house price index updates, and regional market trend data all affect GDV. Applying these to the portfolio continuously means the lender always knows what the GDV looks like under current conditions, not just conditions at origination. Stress-testing at 5%, 10%, and 15% GDV haircuts gives a live view of which facilities are at risk under different market scenarios.

The risk weight consequence

Under Basel 3.1 PS1/26, ADC exposures that meet the Article 124K conditions carry a 100% risk weight. Those that don't carry 150%. The conditions include LTV thresholds tied to the value of the completed development.

If GDV drifts during the loan and the real LTGDV exceeds the Article 124K threshold, the exposure should be reclassified at 150%. A lender who is not monitoring GDV continuously may be holding that exposure at 100% risk weight based on a stale origination valuation. Under a SREP review, that's an evidence problem.

| Scenario | Origination GDV | Month 9 GDV (market -8%) | LTGDV impact |

|---|---|---|---|

| Loan: £2m, GDV: £3m | LTGDV 66.7% | GDV now £2.76m, LTGDV 72.5% | Approaching covenant threshold, risk weight review needed |

| Loan: £2m, GDV: £2.8m | LTGDV 71.4% | GDV now £2.576m, LTGDV 77.6% | Covenant breached, reclassification to 150% risk weight required |

| Loan: £1.5m, GDV: £2.5m | LTGDV 60% | GDV now £2.3m, LTGDV 65.2% | Still compliant, buffer reduced, monitor closely |

What the reporting looks like

Summary

- Every ADC facility is underwritten against a GDV set at origination. The market moves continuously after that. The lender typically doesn't revalue until a trigger event, which may be months after the drift has begun.

- GDV drift creates three hidden risks: LTGDV covenant drift, Article 124K eligibility erosion, and exit assumption risk at the back end of the loan.

- Continuous market monitoring does not require frequent RICS revaluations. Land Registry comparables, local planning data, and macro stress-testing applied to the live portfolio give a continuous GDV picture at low cost.

- The risk weight consequence is concrete: a lender holding an exposure at 100% risk weight based on a stale GDV, when the real LTGDV has drifted above the Article 124K threshold, has a capital adequacy and SREP evidence problem.

- Seeing GDV drift during the loan means having options: early sales, price adjustment, facility restructure. Seeing it at exit means the options have already expired.

Monitor GDV across your portfolio

Mintstone applies live market data to every facility's GDV assumption continuously. LTGDV updates automatically as comparables change. Covenant drift is flagged before a formal revaluation is triggered.

See how it works →